Family disputes over inheritance and wealth distribution are not uncommon, particularly in India where personal laws, diverse family structures, and complex asset portfolios can make estate planning a sensitive issue.

Trusts play a pivotal role in avoiding such disputes, offering a legal framework to manage and distribute assets while minimising potential conflicts.

This article explores the concept of Trusts, their role in estate planning, and how they can help Indian families preserve harmony and secure their financial legacies.

What Is A Trust?

A Trust is a legal arrangement where the owner of assets (the settlor) transfers them to a Trustee for the benefit of one or more individuals, known as Beneficiaries.

The Trustee is tasked with managing the Trust in accordance with the terms outlined in a legal document.

Key Components of a Trust

- Settlor: The person who creates the Trust.

- Trustee: The person or entity responsible for managing the Trust.

- Beneficiaries: Individuals or entities entitled to receive benefits from the Trust.

- Trust Assets: The assets placed into the Trust.

- Trust Deed: The legal document outlining the terms of the Trust.

Types Of Trusts In India

Understanding the different types of Trusts is essential for effective estate planning.

Some common types include:

1. Revocable Trusts

- Definition: A Trust that can be altered or revoked by the settlor during their lifetime.

- Benefits: Flexibility to update terms as circumstances change.

- Example: A Living Trust used to manage assets while the settlor is alive.

2. Irrevocable Trusts

- Definition: A Trust that cannot be modified once established.

- Benefits: Offers greater protection against creditors and tax benefits.

- Example: Trusts set up for asset protection or charitable purposes.

3. Living Trusts

- Definition: Created during the settlor's lifetime.

- Benefits: Allows the settlor to retain control while providing a seamless transition of assets.

4. Testamentary Trusts

- Definition: Established through a Will and activated after the settlor's death.

- Benefits: Ensures asset distribution as per the settlor's wishes.

How Trusts Prevent Family Disputes

1. Clarity in Asset Distribution

The terms of the Trust provide clear instructions for distributing assets, leaving no room for ambiguity. Beneficiaries understand their entitlements, reducing conflicts.

2. Protection of Vulnerable Beneficiaries

Trusts can safeguard assets for Beneficiaries who may be minors, have special needs, or lack financial discipline.

For example:

- Minor children: A Trust can allocate funds for their education and upbringing.

- Special needs Beneficiaries: A special needs Trust ensures they receive support without jeopardising government benefits.

3. Avoiding Probate

A Trust is a legal document that allows assets to bypass probate court, avoiding delays and public scrutiny. This privacy reduces the likelihood of disputes among family members.

4. Customisable Terms

Trusts can be tailored to meet specific family dynamics, such as:

- Allocating funds to support dependents.

- Setting conditions, like age or milestones, for Beneficiaries to access assets.

5. Appointing Neutral Trustees

A Trustee acts as a neutral party to manage the Trust, reducing tensions among family members. Professional Trustees can further ensure impartiality.

Steps To Set Up A Trust In India

1. Identify the Purpose of the Trust

Decide the objectives, such as asset protection, tax efficiency, or providing for dependents.

2. Choose the Type of Trust

Select a revocable or irrevocable Trust, depending on your goals.

3. Draft the Trust Deed

A Trust Deed is a legal document that outlines:

- The purpose of the Trust.

- Details of the settlor, Trustee, and Beneficiaries.

- The assets included in the Trust.

- Terms and conditions for asset distribution.

4. Appoint a Trustee

Select a trustworthy individual or professional entity to manage the Trust.

5. Transfer Assets to the Trust

The settlor transfers ownership of assets such as real estate, bank accounts, or mutual funds to the Trust.

6. Register the Trust

Register the Trust under the Indian Registration Act, 1908, particularly if it involves immovable property.

Tax Implications Of Trusts

1. Income Tax

- Income generated by the Trust may be taxed in the hands of the Beneficiaries or the Trustee, depending on the Trust type.

2. Estate Tax

While India does not currently impose estate duty, Trusts can help minimise other tax liabilities.

3. Gift Tax

Transfers to a Trust may be subject to gift tax regulations under the Income Tax Act.

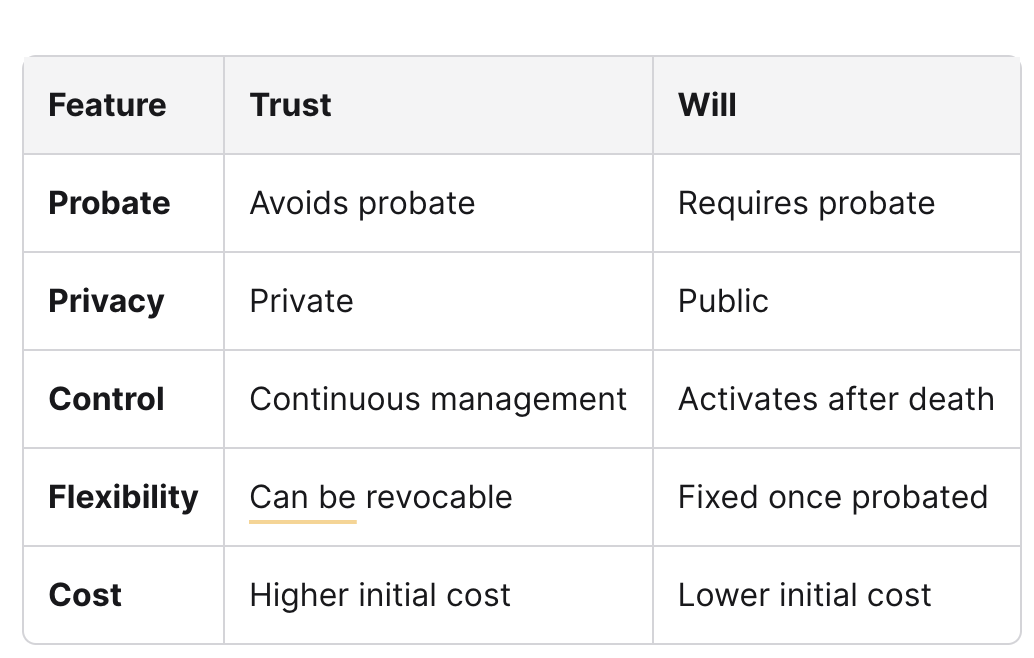

Trusts vs Wills: Which Is Better?

Common Mistakes To Avoid

- Choosing Unreliable Trustees

- Select someone trustworthy and competent.

- Failing to Update the Trust

- Regular updates ensure the Trust reflects current wishes and assets.

- Ignoring Tax Implications

- Work with professionals to understand the tax consequences.

- Not Registering the Trust

- Registration ensures legal validity, especially for immovable property.

FAQs

1. What is the role of the Trustee in a Trust?

The Trustee manages the Trust assets and ensures they are distributed as per the settlor's wishes.

2. Can I set up a Trust for charitable purposes?

Yes, a charitable Trust allows you to support causes while receiving tax benefits.

3. Are Trusts recognised under Indian law?

Yes, Trusts are governed by the Indian Trusts Act, 1882 and related laws.

4. How do Trusts help in estate planning?

Trusts ensure clear asset distribution, protect vulnerable Beneficiaries, and offer tax efficiency.

The Bottom Line: How Yellow Can Help

Trusts are a powerful tool in estate planning, offering flexibility, security, and clarity in asset management and distribution.

In the Indian context, they are especially valuable for avoiding family disputes, safeguarding vulnerable Beneficiaries, and ensuring compliance with legal requirements.

By understanding the nuances of Trusts and working with estate planning professionals, families can preserve their legacies while maintaining harmony.

Take the time to explore how a Trust can benefit your estate plan and secure a future free of conflicts.

At Yellow, we can help you with all aspects of estate planning, including Wills, Trusts, Powers of Attorney, Gift Deeds, Legal Heir and Succession Certificates, and Living Wills. We also offer post-demise and asset transfer services. Our team of legal experts has more than 50 years of combined experience.